-

-

275 Hess Boulevard

Directions

Lancaster, PA 17601 -

Call

717.560.8300 -

Fax

717.833.6303

- contact us

News

The Horizon Beyond Our Sight

Posted on: June 3, 2026

![]()

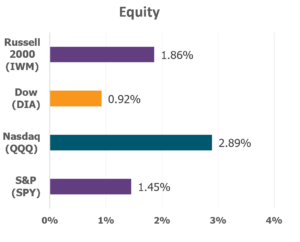

The holiday-shortened week brought another ascent for U.S. equities, as several major indexes climbed to fresh record highs. Investors found encouragement in signs of progress toward a potential peace agreement between the United States and Iran, easing oil prices, and the continued surge of enthusiasm surrounding artificial intelligence. The technology-heavy Nasdaq Composite led the advance, lifted by ongoing confidence in AI-driven innovation, while the Russell 2000, S&P 500, and S&P MidCap 400 also posted notable gains. Even the Dow Jones Industrial Average, though trailing its peers, added a respectable 0.9%. Markets remained closed Monday in observance of Memorial Day, honoring those whose sacrifices have safeguarded the freedoms we often take for granted.

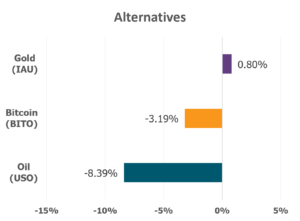

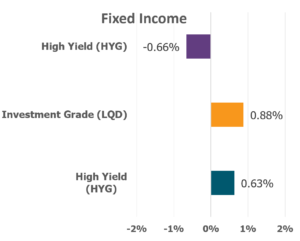

Weekly Performance

Data Source: Factset® Performance Period: 5/25/26 to 5/29/26

For much of the week, the financial landscape seemed illuminated by reports that the United States and Iran were moving closer to extending a ceasefire and restoring traffic through the Strait of Hormuz. As hopes for calmer waters grew, oil prices retreated and investor optimism strengthened. While reports of renewed U.S. strikes on Iranian targets briefly cast shadows across the narrative, confidence endured as indications emerged that a broader agreement was largely complete and awaiting final approval.

Economic data painted a picture of both promise and caution. The Bureau of Economic Analysis reported that its preferred inflation gauge, the Personal Consumption Expenditures (PCE) Price Index, rose 0.4% in April, slower than March’s increase. Yet on an annual basis, inflation accelerated to 3.8%, marking its highest level in nearly a year. Core inflation, which excludes food and energy costs, showed some moderation month over month but still registered its strongest annual reading since late 2023. Meanwhile, personal spending advanced modestly while personal income remained largely unchanged.

Federal Reserve officials continued to sound notes of vigilance. Several policymakers emphasized that inflation’s embers have not been fully extinguished and warned that energy markets, supply chain pressures, and uncertainties surrounding AI-driven productivity gains could yet influence the outlook. The message was clear: while progress has been made, the work is not finished.

Elsewhere, economic signals arrived with mixed tones. First-quarter economic growth was revised lower than initially estimated, reflecting softer consumer spending and investment. Nevertheless, growth remained stronger than the previous quarter, aided by increases in government spending and exports. Durable goods orders provided a brighter headline, rising sharply in April thanks to a surge in transportation equipment demand, though business investment indicators revealed some hesitation beneath the surface.

Sector performance told a story of shifting currents. Energy and Financials faced meaningful declines, falling 5.4% and 5.3%, respectively. In contrast, Technology continued to command attention, advancing 4.6% as investors poured resources into the expanding possibilities of artificial intelligence.

There is a familiar tension in markets during seasons such as these. Headlines speak of peace and conflict, inflation and growth, caution and optimism—all appearing side by side like clouds and sunlight sharing the same sky. Yet such moments remind us that uncertainty has always been part of the human experience. The future remains beyond our sight, but it is never beyond God’s. While markets measure expectations and forecasts seek clarity, faith calls us to remember that true confidence does not originate from economic reports or record highs, but from the One who governs both times of abundance and seasons of questioning. As investors watched indexes reach new heights beneath a horizon still marked by unanswered questions, they witnessed a timeless reality: even when the world weighs possibilities, God remains the author of outcomes yet unseen.

“For now we see through a glass, darkly; but then face to face: now I know in part; but then shall I know even as also I am known.” — 1 Corinthians 13:12

Sources: Yahoo Finance, Reuters.com, and JP Morgan Market Insights

Sources: Yahoo Finance, Reuters.com, and JP Morgan Market Insights. Securities offered through Osaic Wealth, Inc. member FINRA/SIPC. Investment advisory services offered through Faithward Advisors LLC. Osaic Wealth is separately owned and other entities and/or marketing names, products or services referenced here are independent of Osaic Wealth. Dream More, Plan More, Do More is a registered trademark of Faithward Advisors, LLC, Reg. U.S. Pat. & Tm. Off. Any opinions expressed in this forum are not the opinion or view of Faithward Advisors or American Portfolios Financial Services, Inc. (APFS). They have not been reviewed by either firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors.