-

-

275 Hess Boulevard

Directions

Lancaster, PA 17601 -

Call

717.560.8300 -

Fax

717.833.6303

- contact us

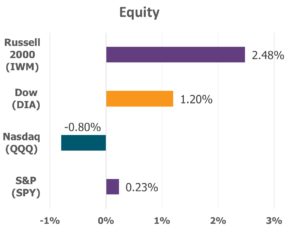

The markets staged a powerful rally last Friday, reversing a downward drift that had burdened the S&P 500 with a five-session losing streak. The Dow emerged as the week’s leader, surging 1.6% and celebrating its first record high of 2025. The S&P 500 managed to end fractionally higher, while the Nasdaq slipped modestly, as investors weighed both uncertainty and hope in the days ahead.

Data Source: Factset® Performance Period: 8/18/2025 to 8/22/2025

Friday’s strength found its spark in Jackson Hole, Wyoming, where Federal Reserve Chair Jerome Powell addressed the central bank’s annual gathering. His words carried both caution and anticipation. Speaking of a labor market caught in what he called a “curious balance,” Powell observed that both supply and demand for workers are softening, with the unemployment rate holding steady at a resilient 4.2%. Yet he warned that downside risks are growing and could materialize swiftly, highlighting the Fed’s rationale for considering a rate cut at its upcoming September 16–17 meeting. The impact of Powell’s remarks was immediate. Market expectations for a September rate cut surged, with futures pricing in an 83.1% probability of a quarter-point reduction by week’s end, according to CME Group’s FedWatch tool. Investors read Powell’s tone as a clear sign that the Fed may act decisively in the weeks ahead to cushion the economy from potential weakness.

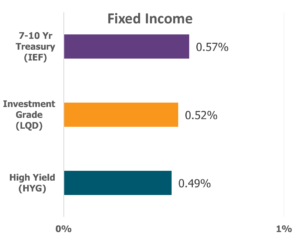

Treasuries responded with measured strength. Bond prices edged higher, pulling yields lower as expectations of easing policy took firmer root. The 2-year Treasury yield experienced the most notable decline, finishing at 3.69%, down from 3.79% the day before. The 10-year Treasury also softened, ending near 4.26% on Friday. For investors, the movement in yields reflected a growing conviction that monetary policy could soon shift toward support rather than restraint.

All eyes now turn to the days ahead, with particular attention fixed on August 29, when the latest reading of the Personal Consumption Expenditures Index (PCE) will be released. As the Fed’s preferred inflation gauge, this data will weigh heavily on the September policy decision. The June release revealed PCE inflation running at an annual rate of 2.6%, the highest in four months. Stripped of food and energy, core inflation stood at 2.8%, underscoring that while price pressures have cooled from their peaks, they remain a lingering concern.

Within the broader market, leadership came from cyclical sectors, underscoring investor optimism in areas tied to economic momentum. Energy stocks surged 2.8% on the week, the strongest sectoral advance, followed closely by Real Estate with a 2.4% gain. Financials and Materials each added 2.1%, demonstrating resilience across industries sensitive to growth. In contrast, Technology shares stumbled, falling 1.6%, while Communication Services declined 0.9%, marking the only two sectors ending the week in the red.

As we continue to steer through the twists and turns of the market and prepare for pivotal weeks ahead, one truth should keep our eyes fixed on what lies ahead: our ultimate confidence is not anchored in market moves, policy shifts, or economic cycles, but in the eternal steadiness of God’s hand. Markets may sway, data may surprise, and forecasts may falter—but the promises of the Lord stand firm. “You will keep in perfect peace those whose minds are steadfast, because they trust in you” (Isaiah 26:3).

Sources: Yahoo Finance, Reuters.com, and JP Morgan Market Insights

Sources: Yahoo Finance, Reuters.com, and JP Morgan Market Insights. Securities offered through Osaic Wealth, Inc. member FINRA/SIPC. Investment advisory services offered through Faithward Advisors LLC. Osaic Wealth is separately owned and other entities and/or marketing names, products or services referenced here are independent of Osaic Wealth. Dream More, Plan More, Do More is a registered trademark of Faithward Advisors, LLC, Reg. U.S. Pat. & Tm. Off. Any opinions expressed in this forum are not the opinion or view of Faithward Advisors or American Portfolios Financial Services, Inc. (APFS). They have not been reviewed by either firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors.

275 Hess Boulevard

Lancaster, PA 17601

Call

717.560.8300Fax

717.833.6303